Mexico’s grid has been in a dire state. In 2024, Mexico’s state-owned utility, CFE, declared 104 individual grid emergencies, including 4 nation-wide grid emergencies in the summer season alone, causing power outages to hit roughly two thirds of Mexico's 32 states.

Reserve margins at Mexico’s grid operator, CENACE, fell to roughly 3% in May 2024 (lower than the regulatory floor of 6%), and losses in the Jalisco industrial corridor from a single outage event were estimated at US$12–15 million. Nationally, manufacturing losses during major outage events can run as high as $200M per hour.

The problem isn't limited to blackouts. Voltage sags, micro-interruptions, and surges cause CNC machines to lose positioning data, robotics controllers to fault, and PLCs to reset mid-cycle. These costs surface in scrap rates and maintenance logs, even if they don’t appear in outage statistics.

Meanwhile, over 60% of the national transmission network already operates near maximum capacity, and electricity demand has been growing at 3.5% annually. These pressures only intensify as nearshoring corridors expand and AI data center development accelerates industrial energy demand in the north and center of the country.

The Institute of the Americas puts it plainly: Mexico's electricity sector is approaching a critical inflection point where rising demand, climate pressures, and declining investment threaten the reliability and competitiveness of the entire power system. Transmission losses remain above 12% of net consumption, forcing additional generation to compensate for wasted energy.

Mexico's electricity sector is approaching a critical inflection point where rising demand, climate pressures, and declining investment threaten the reliability and competitiveness of the entire power system.

A Return to State Primacy in Mexico’s Electricity Sector

The Sheinbaum administration has responded with a sweeping set of reforms and a large public investment commitment. CFE is now required to generate at least 54% of Mexico's total electricity supply, shifting the sector back toward state primacy after years of incremental private-sector expansion.

An independent regulator, the CRE, has been eliminated and replaced by the new National Energy Commission (CNE), which will oversee tariffs and market supervision. Exactly how private investment will be promoted under the new structure remains an open question.

The financial commitment behind this is substantial. CFE's 2024–2030 investment plan totals US$23.4 billion:

- US$12.3B for roughly 13,000 MW of new generation capacity

- US$7.5B to reinforce the national transmission grid

- US$3.6B for distribution infrastructure

A separate US$8.2 billion transmission expansion plan running 2025–2030 targets northern manufacturing corridors, with 58 projects across 25 states planned for 2026 and 2027.

Mexico’s Ministry of Energy, SENER, projects that peak demand will grow 50.6% by 2039, reaching over 83,600 MW, making the current generation gap a structural challenge rather than a cyclical one.

SENER’s plan envisions 19,954 MW of new renewable capacity and 5,000 MW of storage by 2030 alone, with solar PV accounting for 58% of new clean capacity, wind 22%, and BESS the remaining 20%.

Mexico’s Ministry of Energy, SENER, projects that peak demand will grow 50.6% by 2039, reaching over 83,600 MW, making the current generation gap a structural challenge rather than a cyclical one.

Why Energy Storage is Booming in Mexico

Perhaps the most significant structural shift in the new framework is the mandatory co-location of storage with new renewable generation. All new wind and solar projects are now required to include BESS equivalent to 30% of installed capacity, with a minimum three-hour discharge duration.

The project pipeline is already materializing. In December 2025, SENER awarded 3.3 GW of renewable capacity, with every winning project co-located with BESS. The two largest, the 694 MW La Alegría and 351 MW La Esperanza solar projects in Campeche, are being developed by Sunstone Power and include 178 MW and 86 MW of battery energy storage, respectively.

Now, SENER has opened the next round. A new "Call for Strategic Projects" published in May 2026 runs a project registration window from May 25 through August 25, compressing what typically takes 12–24 months into a fast-track approval pathway for projects aligned with national grid planning. The call includes illustrative storage targets across seven regions totaling 935 MW of 3-hour systems, with the North (245 MW), Eastern (180 MW), and Northwest (160 MW) regions representing the largest identified needs.

Projects that partner with CFE through the mixed development scheme receive priority coordination with grid operators and streamlined regulatory treatment.

All new wind and solar projects are now required to include BESS equivalent to 30% of installed capacity, with a minimum three-hour discharge duration.

The Private Sector's Role in Mexico’s Grid Upgrades, and Its Limits

Private investment is explicitly part of the plan, but within a newly constrained structure. Up to 46% of generation can come from private participants, expected to add 6,400–9,550 MW of renewables by 2030 to meet nearshoring demand for clean energy and competitive prices.

Three participation models are available:

- Long-term production contracts (selling exclusively to CFE)

- Mixed investment structure (54% state / 46% private)

- Open market generation with an interconnection contract

The challenge is execution. CFE's balance sheet is already stretched: its debt rose from US$23 billion (1.83% of GDP) in 2018 to US$55 billion (3.07% of GDP) by 2023. CFE’s 2026 budget is 16.7% lower in real terms than 2025, creating direct tension: with less public investment available, private capital becomes increasingly essential to guarantee supply.

And the hardware supply chain won't wait. Power transformers and interconnection equipment carry delivery times of 18–36 months. Battery manufacturers are simultaneously prioritizing projects with the most advanced development status, introducing competitive pressure on production capacity.

The government's own targets — CFE’s plans for 2,216 MW of BESS by 2030 and the PLADESE projection of 8.4 GW of storage through 2038 — will test whether regulatory clarity can translate into physical deployment at scale.

CFE’s 2026 budget is 16.7% lower in real terms than 2025, creating direct tension: with less public investment available, private capital becomes increasingly essential to guarantee supply.

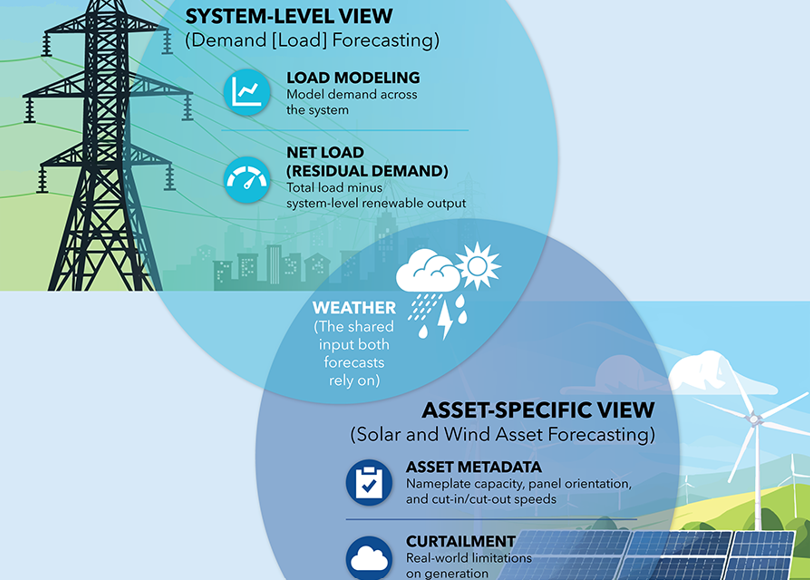

Why Forecasting Helps Mexican Market Participants Navigate a Changing Grid

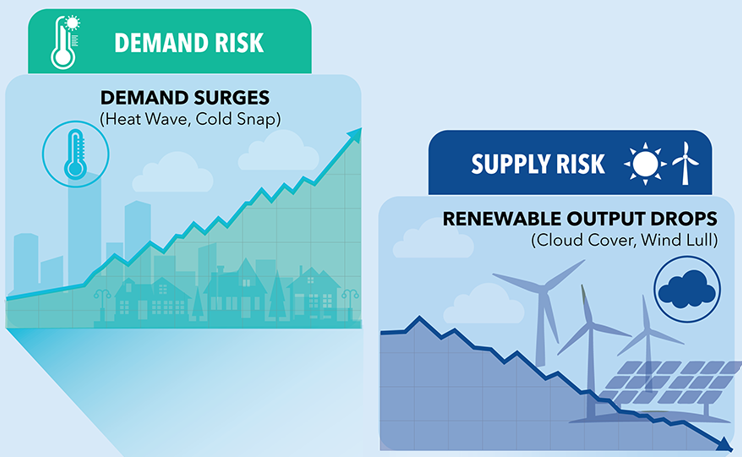

When a grid is simple and slow-moving, rough estimates are sufficient. When it’s in transformation, the cost of being wrong goes up sharply. Mexico is firmly in the second category, adding gigawatts of variable renewables across regions where over 60% of transmission already runs near maximum capacity. It is also absorbing surging nearshoring and data center load all at once.

New generation doesn't just add supply; it reshapes flow patterns across a network that is already congested, creating locational price spreads and curtailment risk that didn't exist before. Participants without visibility into where and when those constraints will bind are flying blind in a market that is getting more complex by the month.

The forecasting challenges are layered:

Critical hours and scarcity pricing

As reserve margins tighten and renewables penetration grows, the hours that matter most (peak demand, low wind, high prices) become harder to predict and more expensive to miss. The 2024 summer events demonstrated what happens when reserve margins hit 3%. As the grid evolves, anticipating those stress periods is the difference between capturing the value of a flexible asset and being caught flat-footed.

As reserve margins tighten and renewables penetration grows, the hours that matter most (peak demand, low wind, high prices) become harder to predict and more expensive to miss.

Day-ahead price formation

The DA market is where most commercial decisions are locked in. As 20+ GW of new capacity enters service and the generation mix shifts materially, price formation will become more complex and less anchored to historical patterns. Models calibrated to the old grid will be systematically wrong as the new one emerges.

Price formation will become more complex and less anchored to historical patterns.

Renewables dispatch at scale

With mandatory BESS co-location, every new solar and wind project in Mexico is also a storage optimization problem. Getting the generation forecast right is the prerequisite for dispatching storage correctly, and with 3-hour systems as the standard, the margin for error is measured in minutes rather than hours.

Nearshoring load growth in constrained regions

The Bajío, Nuevo León, and northern border states where manufacturing expansion is concentrated are also the regions where transmission is most constrained. Load growth here won't follow historical patterns. It will be lumpy, industrial, and geographically concentrated in ways that require locational, asset-level forecasting rather than system-level averages.

Load growth here won't follow historical patterns. It will be lumpy, industrial, and geographically concentrated.

Why Mexico’s Grid Transformation Matters Across North America

Mexico's grid transformation is genuinely one of the most significant infrastructure build-outs happening in North America right now. The combination of regulatory modernization, large-scale public investment, mandatory storage integration, and a fast-track permitting pathway creates conditions where new entrants and incumbents alike can compete, if they have the right tools.

The country's success matters well beyond its borders. US supply chains, manufacturing competitiveness, and corporate clean energy sourcing targets all depend on Mexico's ability to provide massive amounts of reliable power while decarbonizing.

Whether President Sheinbaum's reforms succeed could provide a template for other emerging economies. If they fall short, they could endanger nearshoring progress and climate targets across North America.

The participants who will benefit most from this transformation are those who can see it coming: those who know which hours will be scarce, which corridors will be constrained, and which assets will underperform before the dispatch instructions are issued.

US supply chains, manufacturing competitiveness, and corporate clean energy sourcing targets all depend on Mexico's ability to provide massive amounts of reliable power while decarbonizing.

Explore Load Risk Management solutions.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

.avif)

.avif)

.avif)

.avif)