CAISO’s Day‑Ahead Market Enhancements (DAME) take effect May 1, 2026, introducing new settlement exposure for every participant in the CAISO day‑ahead market. Alongside the launch of the Extended Day‑Ahead Market (EDAM), CAISO will begin procuring Imbalance Reserves (IR), a product that directly ties forecast accuracy to cost allocation.

For the first time, the difference between what the market expects and what actually happens will appear as a discrete line item on settlement statements. Forecast uncertainty, long treated as an implicit system burden, will be explicitly priced.

Most industry focus has been on EDAM’s regional expansion. DAME, and Imbalance Reserves in particular, will have the more immediate financial impact.

What Are Imbalance Reserves?

Imbalance Reserves explicitly price the gap between the day‑ahead schedule and real‑time outcomes.

Through Imbalance Reserves, CAISO now measures the gap between expectation and reality and assigns the cost of that gap directly to market participants, rather than absorbing it implicitly through after‑the‑fact reliability actions. Participants who understand these mechanics can actively manage their exposure instead of discovering it after settlement.

More specifically, Imbalance Reserves are a bi‑directional capacity product, procured upward (IRU) and downward (IRD) in the day‑ahead market and co‑optimized with energy and ancillary services. Their purpose is to ensure CAISO has sufficient ramping capability to manage deviations between the day‑ahead net load forecast and actual real‑time net load.

Unlike legacy reserve constructs, IR requirements are sized directly from historical day‑ahead‑to‑real‑time forecast errors, using statistical methods that reflect observed variability. Larger and more volatile forecast errors result in larger IR procurement volumes—and higher costs. In effect, forecast uncertainty is no longer absorbed by the system. Market participants will now incur the costs.

In effect, forecast uncertainty is no longer absorbed by the system. Market participants will now incur the costs.

Why Is CAISO Implementing Imbalance Reserves?

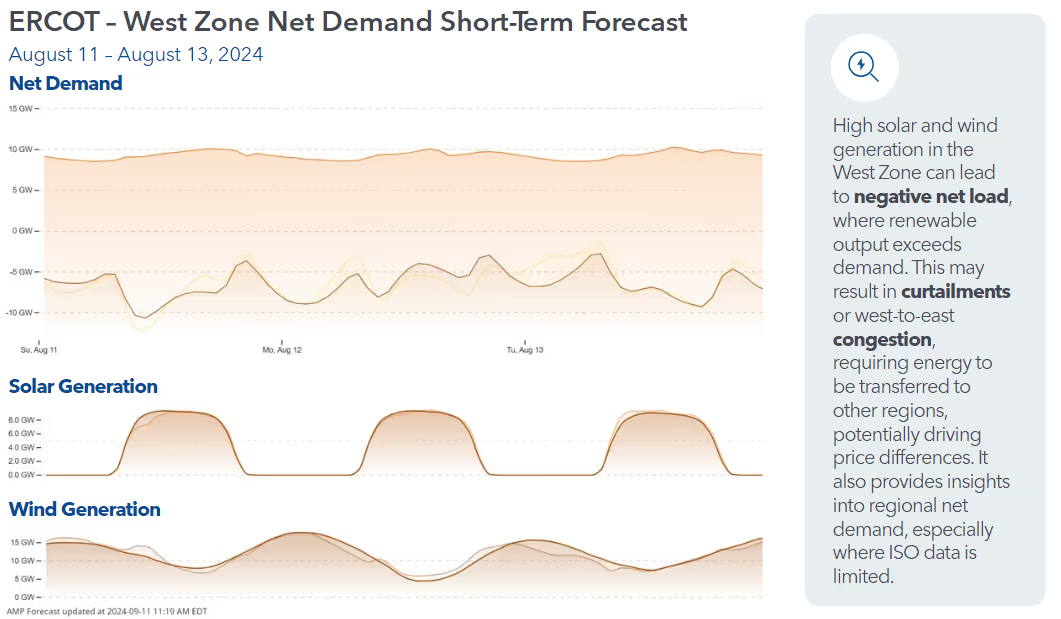

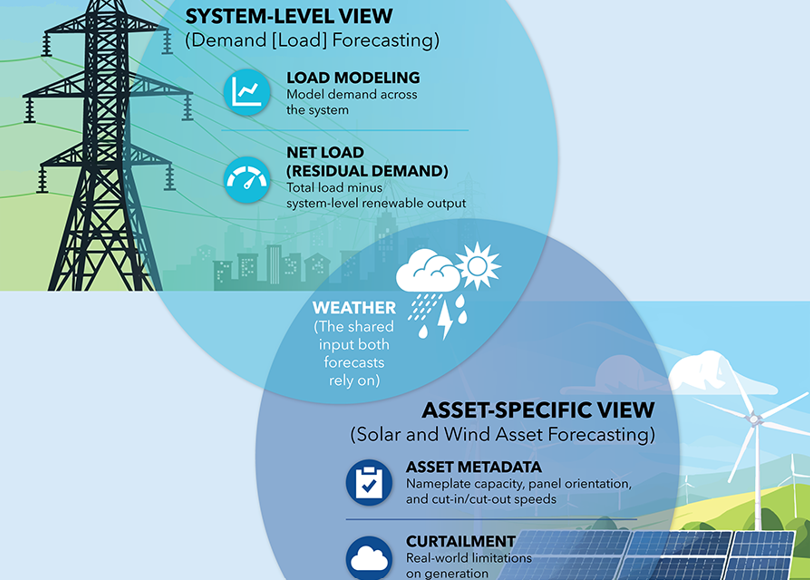

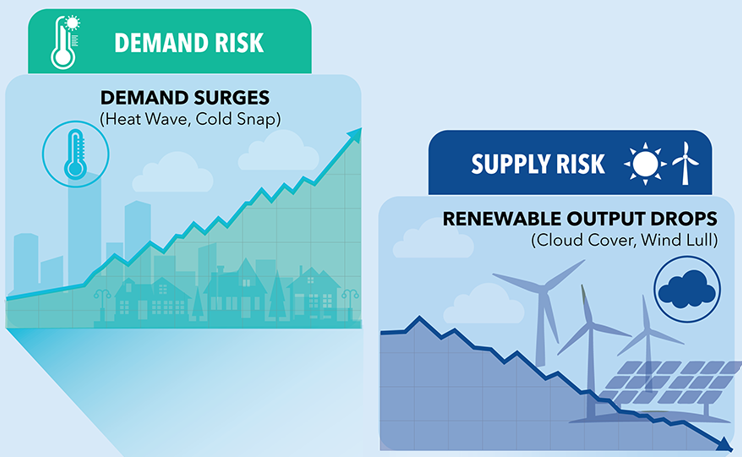

Rapid growth in solar, wind, and battery storage has reshaped CAISO’s net load profile so profoundly that it can no longer manage volatility through traditional commitment tools.

Intra‑hour ramps have steepened, variability has increased, and forecast errors have widened, often compressing system swings into short time windows. Battery charging during midday hours now represents a meaningful share of total load, while evening ramps rely increasingly on fast, flexible resources. These dynamics have pushed processes like Residual Unit Commitment to their limits.

Imbalance Reserves shift that risk earlier in time by procuring ramping capability directly in the day‑ahead market. CAISO explicitly conditioned EDAM’s approval on the availability of IR, viewing geographic diversity and uncertainty management as complementary tools.

Imbalance Reserves shift that risk earlier in time by procuring ramping capability directly in the day‑ahead market.

A New Settlement Line Item with Real Financial Impact

Imbalance Reserves introduce a new, recurring cost that varies by participant behavior. Beginning in May 2026, IR will appear as a distinct settlement charge code on participant invoices. For many organizations—especially Community Choice Aggregators—this represents a cost category they have never had to actively manage before.

IR costs allocated to load follow a two‑tiered structure. Under Tier 1, the participant‑specific component, cost:

- is driven by how much your day‑ahead schedule deviates from actual metered demand

- increases as your contribution to system uncertainty increases

Put simply: greater forecast error produces higher Tier 1 IR charges. Forecast performance now translates directly into settlement dollars. Unlike fixed or broadly socialized charges, a portion of IR costs is behavior‑dependent. Your forecast accuracy now directly influences how much of the Tier 1 IR bill you pay.

Put simply: greater forecast error produces higher Tier 1 IR charges.

What This Means for LSEs, Generators, and Traders

Load‑Serving Entities & Community Choice Aggregators

Reducing demand forecast error is the most effective way to lower Tier 1 IR costs.

For LSEs and CCAs, Imbalance Reserves create a clear incentive alignment. Every improvement in day‑ahead demand accuracy reduces exposure to uncertainty‑based cost allocation.

These reductions appear directly on settlement statements, month after month. Organizations relying on forecasting approaches built for a less volatile, lower‑renewables grid will feel the impact most acutely.

Reducing demand forecast error is the most effective way to lower Tier 1 IR costs.

Generators & Storage Operators

IR creates new revenue opportunities for asset operators, but it also creates new performance and availability risk.

Resources awarded Imbalance Reserves must submit economic real‑time bids for the awarded capacity range and remain available for dispatch. Failure to perform can result in penalties linked to IR or flexible ramping prices.

Battery storage operators are particularly well positioned to provide IR due to their fast, bi‑directional ramping capability. However, IR awards interact with energy dispatch, ancillary services, and state‑of‑charge constraints. Optimizing across those markets requires clear visibility into expected net‑load conditions before the day clears.

IR creates new revenue opportunities for asset operators, but it also creates new performance and availability risk.

Traders

IR procurement tightens the day‑ahead supply stack and reshapes price formation.

When IR requirements are large, capacity that would otherwise clear in the energy market is withheld to meet reserve needs. That tightening alters day‑ahead prices and introduces new signals for convergence and virtual strategies.

High‑uncertainty conditions—cloud variability, regional weather divergence, or extreme ramps—are exactly when these effects are most pronounced. Participants who can anticipate those days can position ahead of the market rather than reacting after the fact.

Participants who can anticipate [high-uncertainty] days can position ahead of the market rather than reacting after the fact.

How to Manage Imbalance Reserve Costs

Every dimension of Imbalance Reserves ultimately traces back to forecast quality. For load‑serving entities and CCAs, tighter demand forecasts directly reduce Tier 1 IR costs. For traders and asset operators, identifying when the day‑ahead‑to‑real‑time gap will widen allows for earlier, more informed positioning.

EDAM will expand, more participants will join, and the IR cost pool will grow. Those who manage forecast uncertainty intentionally will gain a structural advantage. Those who don’t will learn what it costs starting in May.

As Mae West once put it: “A dame that knows the ropes isn’t likely to get tied up.”

Book a demo to see why Amperon leads the industry in forecast accuracy.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

%20(10).avif)

.avif)

.avif)

.avif)

.avif)