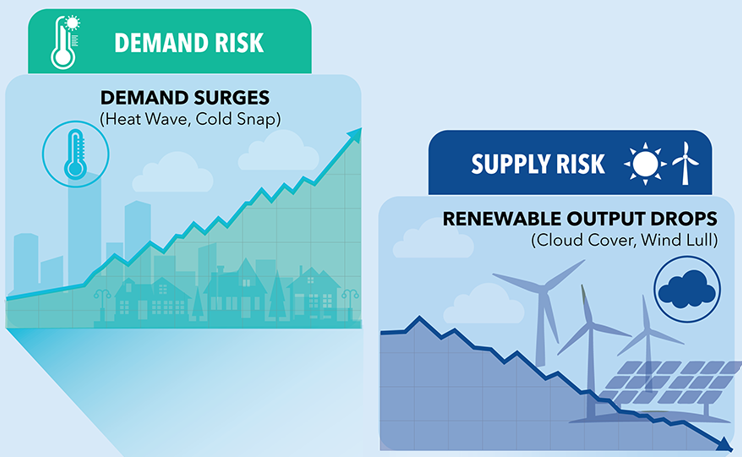

Conventional wisdom says that European power markets don't respond to summer heat the way American ones do, but that’s beginning to change. Air conditioning penetration across the continent has grown rapidly over the last seven years, gas storage is entering the season well below historical norms, and the ECMWF's latest seasonal forecast is calling for temperatures as much as 1.5°C above normal across much of the continent, concentrated in Southern Europe but extending northward through the summer months. The last El Niño of comparable magnitude hit in 2015, and a warming climate means the baseline keeps rising.

What makes this summer different is not the prospect of a single extreme heat event, but the potential for sustained, prolonged heat. European homes and buildings are slow to heat up but equally slow to cool down. Once urban centers become heat sinks, overnight temperatures can stay above 20°C for days. At that point, air conditioning demand stops being elastic and starts being structural, and the grid feels it in ways that are difficult to hedge. Depending on the market, a sustained heat wave can add between 6 and 16% to electric demand, comparable to winter peak heating loads in some regions.

Amperon is tracking three main risks:

Nuclear Curtailment in France

France has historically been a stabilizing force in European power markets, exporting reliable nuclear baseload to its neighbors. This summer, that dynamic is at risk of reversing.

The mechanism is straightforward but easy to underestimate. When river temperatures rise too high, or water levels too low, French nuclear plants on the Rhône face environmental limits on cooling water discharge, triggering regulatory curtailment even when the cooling technology itself could still operate.

France is not immune to demand-side pressure either. If three or more consecutive days of elevated demand coincide with nuclear supply constraints, the system will face meaningful stress on the supply stack. In that scenario, France could become a net importer, with price implications that would ripple across interconnected markets.

Demand Spikes in Italy and Spain

Italy is the clearest case of a market that has structurally changed without structurally preparing. Its all-time system peak was set during the 2015 El Niño, when air conditioning penetration hovered around 7%. Today, that figure is approaching 50%. And climate change only adds fuel to the fire.

The supply picture offers little relief. Italy has seen among the slowest renewable capacity growth in Western Europe in recent years. It remains a heavily gas-driven marginal price market. An extended demand shift of 3 to 7 GW, within the range observed during past Italian heat events, would translate directly to higher gas burn, competing with storage operators trying to refill reserves heading into winter.

Spain faces a similar demand picture, with approximately 5 GW of potential incremental load during a prolonged heat event, but a meaningfully different supply profile. Rapid solar buildout over the past six years has changed the market's midday dynamics considerably, but residual demand could exceed 10 GW during sustained heat, stressing the system especially during shoulder hours.

El Niño also tends to correlate with below-average wind generation across Iberia. Spanish wind output peaked near 20 GW earlier this year, but has already weakened materially through spring, with most April generation staying below 10 GW. In a heat event, Spain cannot rely on wind to provide the buffer it might in a cooler, windier summer.

Gas Burn Could Affect Winter Storage

The third risk is the one with the longest tail. European natural gas storage entered this summer at roughly 36% fill, well below both the five-year average and the levels required to comfortably meet winter demand. Add in the ongoing geopolitical complications around Middle Eastern LNG supply, and the path to full storage heading into winter gets narrower still.

Germany is something of a counterweight here. Rapid solar growth, both grid-scale and rooftop, combined with relatively modest air conditioning adoption positions Germany to be a net power exporter this summer, potentially supporting adjacent markets during heat events and absorbing some of the pressure that would otherwise fall on gas-fired generation.

Germany’s strong grid connectivity and growing battery storage fleet make it the most likely source of continental stabilization. But Germany alone cannot fully offset coordinated demand and supply stress across France, Italy, and Spain simultaneously.

The bottom line is that European power markets are heading into a summer where the familiar rules no longer apply. The conventional wisdom that European A/C penetration is too low to matter has not been accurate for several years. The question this summer is how markets respond when that demand shows up at scale, simultaneously across multiple countries, while a key source of baseload supply faces temperature-driven constraints and gas storage sits below the level needed for a comfortable winter.

Download the 2026 European Summer Grid Outlook for a full analysis.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

%20(10).avif)

.avif)

.avif)

.avif)

.avif)