Executive Summary

Global power grids are evolving rapidly. The nature and timing of this evolution look different in every region, but several common themes prevail. Load is growing and ramps are steepening, which in turn incentivizes load flexibility in various forms.

The global generation mix is steadily incorporating more renewable energy, even as coal and nuclear plant retirements remain uncertain. Congestion and curtailment are on the rise, and despite the rapid growth of batteries, long-term energy storage remains elusive.

These trends mean grid operators and market participants must make sense of large and ever-changing data sets to maintain reliability and profitability in the face of increasingly volatile supply and demand dynamics.

Electric Load Trends

Load Growth is Changing Load Profiles

After years of stagnation in many advanced economies, load growth is here to stay. Load growth is the increase in electric demand within a power system or region.

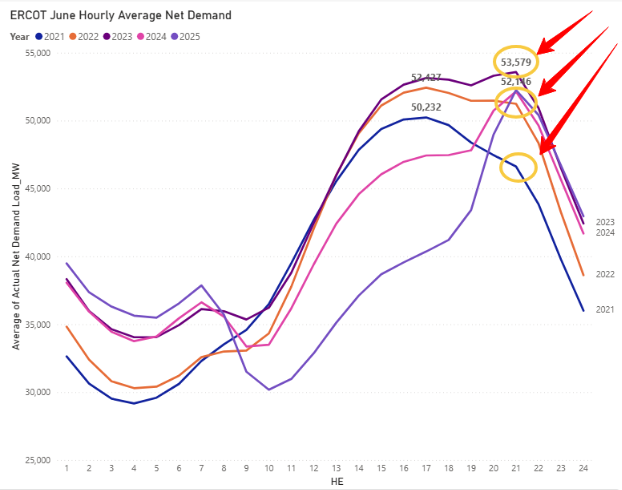

Globally, demand growth leapt from 2.5% in 2023 to 4.3% in 2024—a 72% increase in the growth rate year over year. Just as importantly, load growth is also changing load profiles, often creating higher peaks and steeper ramps.

Driven largely by data centers, baseload power demand is on the rise, even as new baseload capacity additions are slowing dramatically. Even more concerning, though, is the evening ramp period that often coincides with peak air conditioning demand and waning solar output.

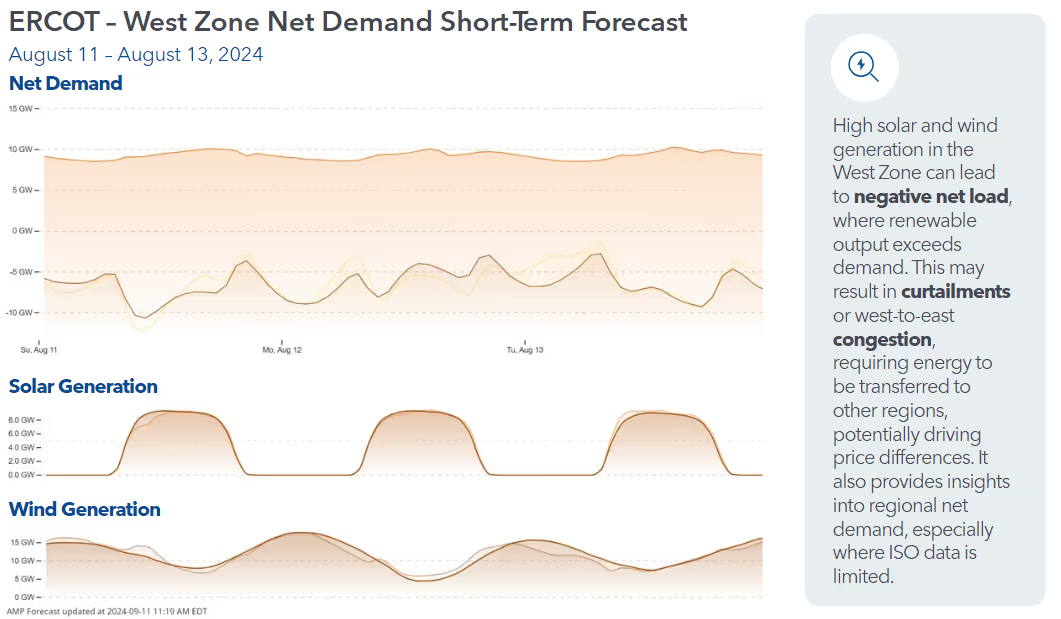

In Texas, for example, summer net demand now consistently peaks around 9:00pm rather than the traditional 5:00pm, with the summer sunset driving a late evening peak. As a result, solar is no longer an adequate hedge against 4CP charges for large commercial and industrial customers.

Load Flexibility Hits a Major Inflection Point

Historically, load was treated as a given. Today, electric demand can be managed in much the same way as supply. Load flexibility is the ability of electricity consumers (including homes and businesses) to adjust their consumption patterns, potentially saving them money while acting as a supporting resource for grid operators in much the same way that a power plant would.

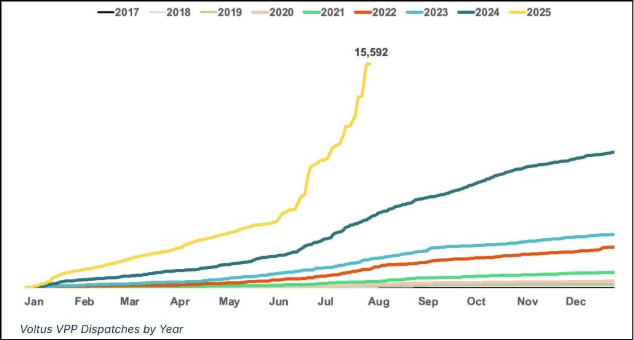

Load flexibility comes in various forms: Virtual Power Plants (VPPs), Demand Response (DR), and other programs that allow utilities to call upon or incentivize load reductions at key times. Demand-side management is not new, but it reached a notable inflection point in 2025.

Nowhere is the need for load flexibility more potent than in data centers. Forecasts now project 106 GW of data center load by 2035, more than four times the 25 GW of operating capacity in 2024, and utilities are struggling to keep up with interconnection requests and new capacity additions.

Even if only a fraction of planned projects materialize, the sheer scale of growth is compressing what used to be a decade-long planning horizon into just a few years, creating bottlenecks, reliability risks, and pressure on transmission and generation resources.

Some balancing authorities like the Southwest Power Pool have proposed interruptible services for large loads. And hyperscalers are on board: Google, for example, announced an initiative to make Machine Learning (ML) demand more flexible in search of faster grid interconnection for new facilities. Expect more initiatives like this in 2026.

Electrical Generation Trends

Renewable Energy Growth Marches On Nearly Everywhere

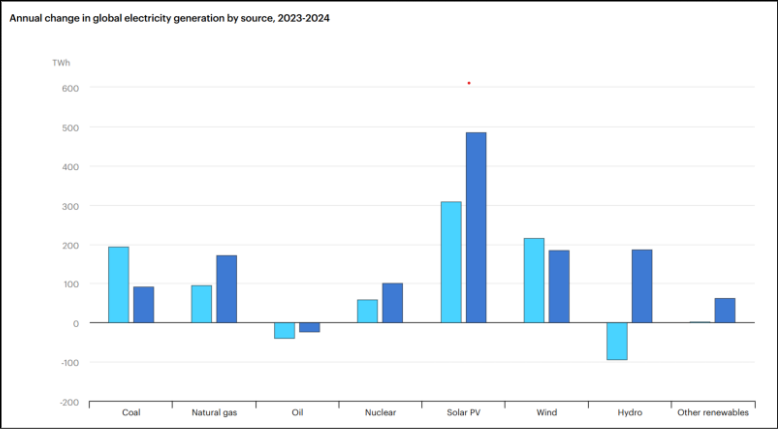

Led by solar PV, nearly 75% of global capacity additions now come from renewable sources. China dominates this growth, but the trend holds true nearly everywhere, including in regions challenged by grid constraints, supply chain constraints, and political backlash.

Source: IEA

Renewable energy growth is not new, but it’s striking to note just how widespread it is:

- India added 25 GW of renewable energy capacity in FY 2024-2025, while its domestic module manufacturing capacity nearly doubled. Despite global supply chain disruptions and land use disputes, India's clean energy growth was 3x higher than load growth in the first half of 2025.

- South Africa’s rooftop solar boom shows how consumer demand can overcome grid and political barriers. Chronic load shedding drove households and businesses to install 6 GW of private PV between 2022 and 2024, doubling installed capacity and lifting solar to nearly 8% of generation despite coal’s dominance.

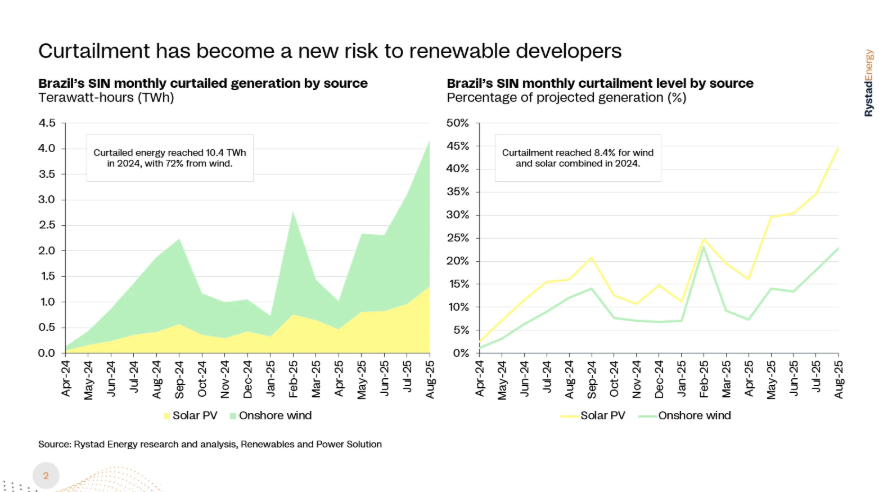

- Brazil scaled solar rapidly, even as curtailment hit 27% in some regions. Distributed generation programs and hybrid projects made Brazil one of the leading solar markets starting in 2024. Together, solar and wind produce nearly a quarter of Brazil's electricity, in addition to over 50% from hydro!

Retirements Continue to Push Capacity Prices Higher

A power plant retirement is the permanent closure and decommissioning of an electric generation facility. In many regions, plants are retiring faster than new generation can be interconnected—even as load growth is spiking. Many retirements have been delayed or canceled to maintain reliability, but even so, capacity market prices are climbing rapidly.

In PJM, for example, the 2025–2026 capacity auction cleared at record-breaking prices, and this winter will be the first under those high rates. Notably, the 2026–2027 auction cleared even higher at $329/MW-day across the PJM footprint. The impact of these elevated prices will be felt on customer bills this winter and likely through at least 2027.

MISO annualized auction prices settled around $215/MW-day, a significant jump from last year and a signal that MISO’s capacity market is increasingly aligning with PJM’s in terms of pricing dynamics and volatility. For the North, Central, and South zones, prices for Summer 2025 cleared at a staggering $666.50, driven by rising demand and a year-over-year decline of roughly 2 GW in surplus capacity.

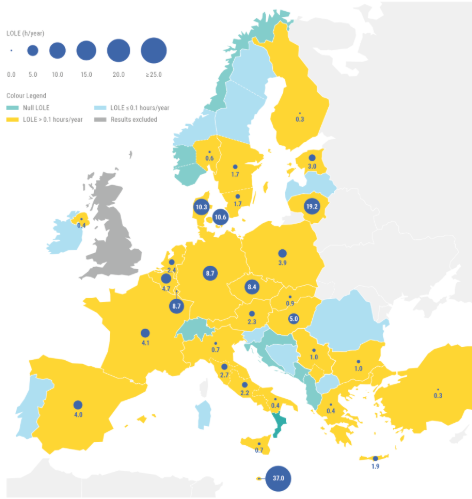

In Europe, as renewables increasingly dominate, fossil fueled plants are becoming uneconomical, leading to accelerating reliability concerns. Germany, for example, is projected to have insufficient capacity for roughly 8 hours in 2026, ramping up to 18 hours in 2028. The European Commission is responding with a plan to fast-track grid projects, among other efforts.

Source: ENTSO-E

Congestion and Curtailment are Accelerating Rapidly

Transmission infrastructure has failed to keep pace with both load growth and renewables supply, often creating severe bottlenecks that cause congestion charges, curtailment, and negative pricing. The scale of this trend is staggering, and while it’s especially severe in certain grids with high penetrations of renewable energy, curtailment risk is rising on every continent.

In the US, many ISOs continue to break records for renewable energy curtailment. Globally, similar patterns are emerging: Germany recorded 457 hours of negative pricing in 2024, and Brazil’s curtailments surged 230% year-over-year, adding up to hundreds of millions in losses for generators.

Source: Rystad Energy

Congestion and curtailment will intensify before they improve. This is not just because renewable supply is rising, but because demand is growing on timelines the grid simply can’t match. This is forcing utilities to compress what used to be ten-year grid plans into three, yet the infrastructure required to support that growth still follows decade-long development cycles.

Transmission lines take seven to ten years to permit and build; substation upgrades span multiple planning cycles; and large transformers now carry two-year lead times. US utilities are planning $84.9 billion in T&D spending in 2025 and developing over 26,000 miles of new transmission, but most of these projects won’t arrive until late in the decade.

The result is widening structural bottlenecks in CAISO’s north–south corridors, ERCOT’s West and Panhandle export paths, and SPP’s wind-heavy plains network—regions seeing record levels of curtailment despite soaring investment.

And with more than 1,350 GW of generation and hundreds of GW of storage sitting in interconnection queues—exceeding the capacity of the entire existing US grid—congestion pressures will continue intensifying through 2026 as load grows faster than transmission, stability resources, and local infrastructure can keep up.

Batteries Are Growing Fast—But Not Fast Enough

Utility-scale batteries—large energy storage systems designed to support the grid—are scaling at an unprecedented pace. Yet even with this rapid growth, battery energy storage remains a fraction of what’s needed to balance grids increasingly dominated by intermittent generation.

Battery energy storage system (BESS) installations are approaching 100 GW a year, with China, the US, and Europe leading the charge. In markets like California, battery capacity has grown from less than 1 GW in 2020 to over 13 GW today. Now ERCOT is catching up, and the rest of North America’s grids will look to follow these examples. Germany, meanwhile, doubled its large-scale storage in 2024 alone. These assets are increasingly paired with renewables, helping absorb midday solar surpluses and mitigate curtailment risk.

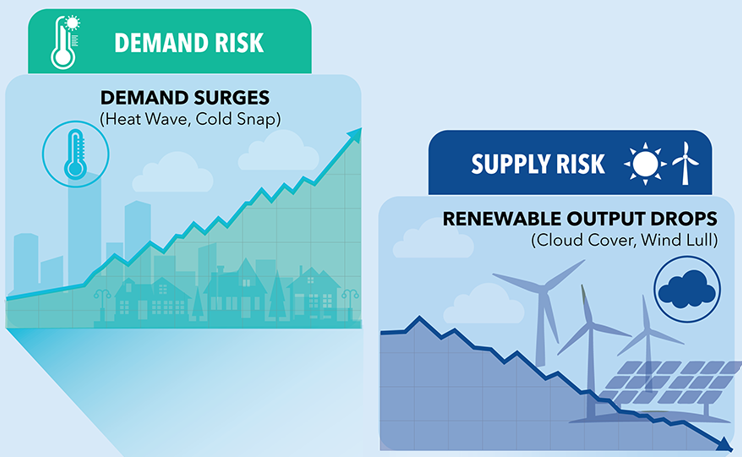

Energy storage is imperative for smoothing short-term volatility, yet it cannot replace the role of dispatchable generation during prolonged weather-driven deficits. The challenge lies in the mismatch between renewable variability and battery duration. Most new systems are short-duration—typically 2 to 4 hours—designed for peak-shaving and ancillary services rather than sustained reliability.

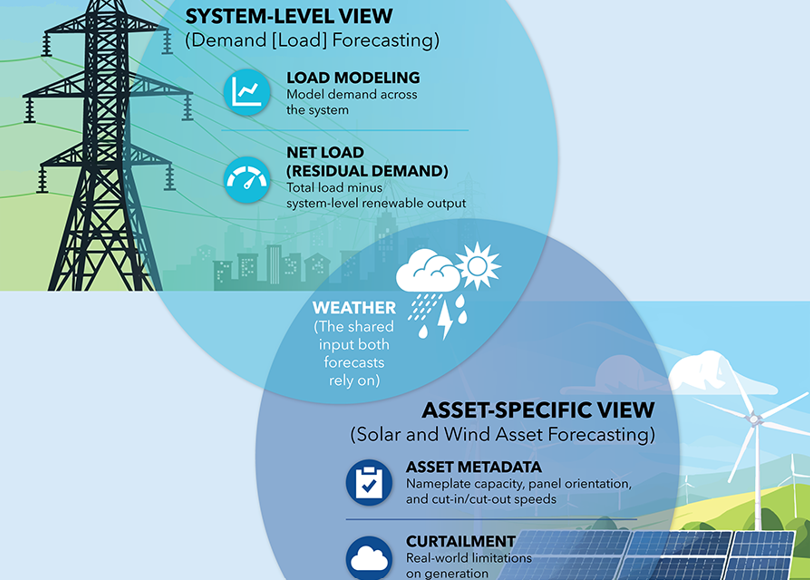

Long-duration storage technologies are advancing, but commercial deployment remains limited. Without a breakthrough in cost and scalability, grids will continue to rely on fossil backup or imports during extended renewable droughts, informed by increasingly robust forecasting for both grid demand and renewables supply.

The Future of the Grid Won’t Wait

The grid of 2026 will be defined by rapid change—driven not only by surging data center demand and ballooning renewable energy curtailment, but also by evolving peak demand hours and a tipping point for load flexibility. Grid operators and market participants who fail to adapt will face mounting costs, reliability concerns, and competitive disadvantages.

These shifts reflect a fundamental transformation in how electricity is consumed and delivered. Evening ramps are steepening as solar output fades, while hyperscale data centers force utilities to compress decade-long planning processes into just a few years. At the same time, distributed resources and demand-side management programs are reshaping the traditional load curve, creating both operational uncertainty and new opportunities for innovation.

These dynamics bring both upside potential and risk. Flexibility programs such as Virtual Power Plants (VPPs) and demand response are moving from niche tools to core grid resources, while transmission bottlenecks and the lack of long-duration storage remain critical constraints. Congestion and curtailment are accelerating globally, and short-duration batteries, though growing fast, cannot fully bridge the reliability gap during prolonged renewable droughts.

Market participants who anticipate these trends through strategic planning, robust forecasting, and adaptive operations will be best positioned to thrive. Accurate insights into load growth, renewable variability, and congestion risk will become essential for utilities, traders, and large power users. Those who embrace data-driven decision-making can turn volatility into opportunity, while those who lag behind will struggle to maintain profitability and reliability in an increasingly complex energy landscape.

Grid operators and market participants who fail to adapt will face mounting costs, reliability concerns, and competitive disadvantages.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

%20(10).avif)

.avif)

.avif)

.avif)

.avif)