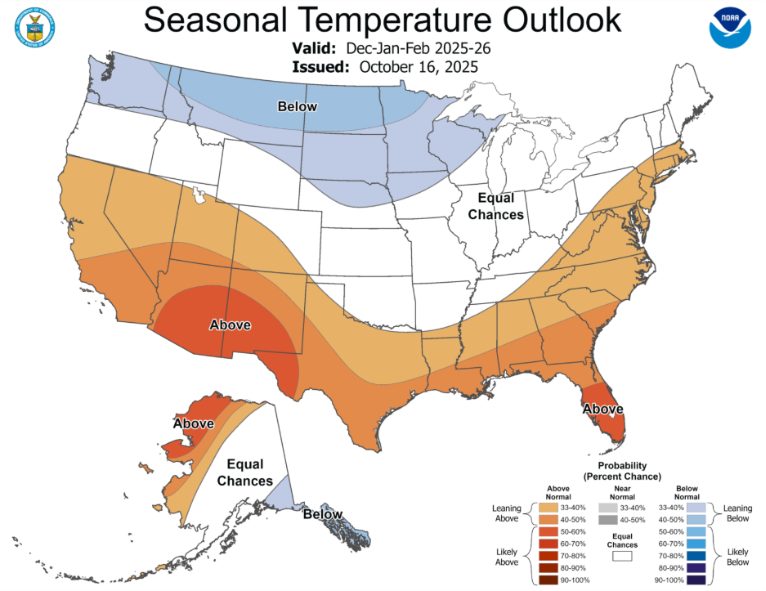

Winter 2025-2026 is looking anything but predictable. Significant weather risks and other market developments could threaten US grids, despite near-normal average temperatures. A neutral to weak La Niña pattern could mean heightened volatility. With no strong weather signal at play, almost anything can happen. Significant cold air outbreaks are possible, despite generally warm and dry conditions across the eastern and southern US.

Expect lake effect snow in the Great Lakes region and cooler and wetter than average conditions in the Pacific Northwest, although the Pacific “blob” could interfere. ERCOT is likely to see another warm and dry winter, yet market developments could lead to more short-term price volatility. Load growth continues to threaten reserve margins across the country, although delays in power plant retirements have been mitigating these effects.

The northern portions of the Midwest and Great Plains are likely to see below-average temperatures and are prime targets for intense cold air outbreaks.

Source: NOAA

US Winter Weather Outlook

This winter is shaping up under a neutral to weak La Niña pattern, similar to last year. Historically, La Niña winters bring warmer, drier conditions to the Southern and Eastern U.S. and cooler, wetter weather to the Pacific Northwest. But weak ENSO signals often mean unpredictability—and last year’s Gulf Coast blizzard was proof that “anything can happen.”

Adding to the complexity:

- Pacific Warm Blob: A persistent zone of warm water could block storms from hitting the West Coast, amplifying cold air outbreaks in the central and eastern U.S.

- Easterly QBO: This atmospheric phase weakens the polar vortex, increasing the odds of sudden stratospheric warming (SSW) events—often precursors to Arctic blasts in the mid latitudes.

Bottom line: uncertainty is the forecast.

A large mass of warm water is lingering in the Pacific, adding further complication to an already volatile US weather forecast.

Source: NOAA

Winter Weather Analysis by ISO

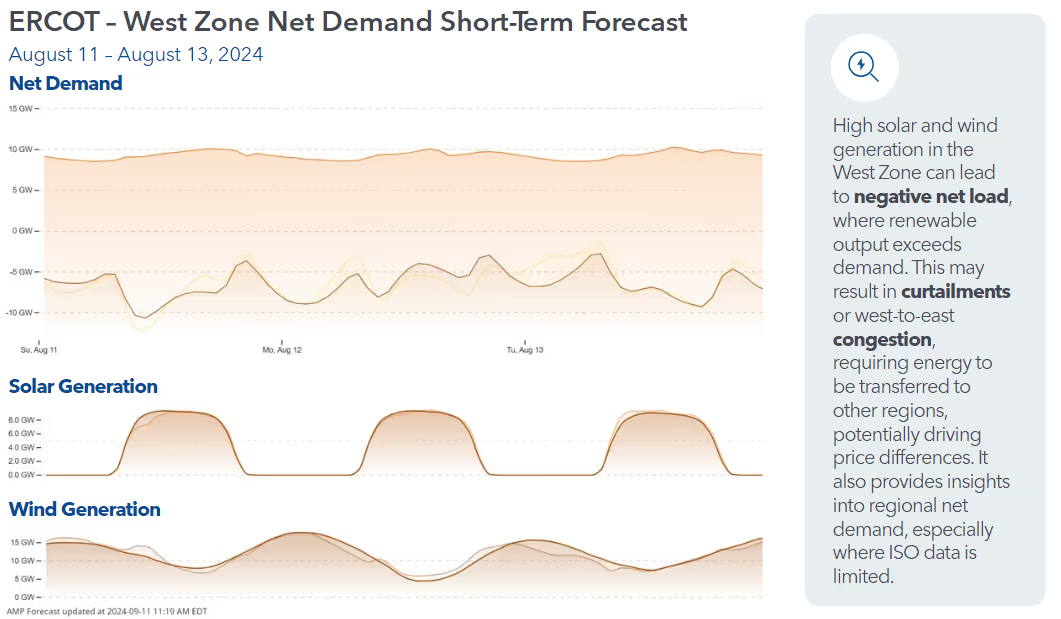

ERCOT: Warm Forecast, Cold Risks

Texas is likely to see a warmer, drier winter, but don’t rule out short-lived Arctic blasts. The good news? ERCOT is better prepared than last year:

- RTC+B Launch: Starting December 5, ERCOT’s new real-time co-optimization system will integrate battery state-of-charge data, improving dispatch efficiency.

- Battery Boom: ERCOT recently hit a record 8.6 GW of battery dispatch, with another 3.7 GW expected by March. Solar capacity is also surging past 30 GW.

Still, expect short-term price volatility during cold snaps as the market adjusts to RTC+B.

ISONE & NYISO: Electrification and Lake Effect Snow

The Northeast is trending warmer than normal, but volatility looms:

- Lake Effect Snow: Great Lakes temperatures are 3–5°F above normal, raising the risk of heavy snow early in the season.

- Electrification Surge: Electric heating adoption has jumped from 35% to 42% of households, pushing winter demand higher. NYISO could become a winter-peaking ISO by 2038.

- New Renewables: Vineyard Wind 1 (800 MW offshore) and Baron Winds II (400 MW onshore) are set to boost supply just in time for Nor’easter season.

CAISO & the Pacific Northwest: Batteries Surge, Snowpack Uncertain

California expects warmer, drier conditions, while the Pacific Northwest braces for colder, wetter weather—though the warm blob could disrupt storm tracks.

- Snowpack Matters: Last year’s below-normal snowpack hurt hydropower. This winter’s outlook is mixed, with competing factors at play.

- Storage Growth: CAISO will add nearly 1 GW of battery capacity this winter, reinforcing grid flexibility as solar curtailment rises.

MISO & SPP: Arctic Threats & Delayed Retirements

Northern areas (Dakotas, Minnesota) face colder, wetter conditions, while the south stays warm and dry. Key themes:

- Retirement Delays: Coal plants like J.H. Campbell and R.M. Schafer have pushed back closures to maintain reliability.

- Renewables & Curtailment: Wind curtailment remains a challenge, especially overnight. Solar additions (3.7 GW across MISO/SPP) could ease midday stress.

PJM: High Prices and Rising Demand

PJM enters winter under record-high capacity prices and growing load forecasts:

- Capacity Auction Impact: Rates cleared at $329.17/MW-day for 2026–2027, driving up customer bills.

- Demand Surge: winter peaks are trending higher, with somePJM’s forecasts suggesting 150 GW+ possible during an Arctic blast.

winter peaks are trending higher year over year, and there is a possibility of surpassing last year’s winter peak.

- Renewables: 1.6 GW of solar expected online by March, strengthening PJM’s resource mix.

US Winter Weather Summary

This winter’s mantra: “Mild on paper, volatile in practice.” Between weak ENSO signals, shifting atmospheric patterns, and evolving grid dynamics, forecasting extremes—not just averages—will define success.

Amperon’s Grid Mid-Term Forecasting (Grid MTF) ensembles already flag potential peak demand events across multiple ISOs. In a world where volatility is the norm, granular insights and real-time adaptability are no longer optional—they’re essential.

Key Takeaways

- Expect surprises: Weak La Niña + easterly QBO = high Arctic blast risk.

- Grid readiness matters: Battery growth and real-time optimization will be tested.

- Electrification is reshaping demand: Especially in the Northeast.

- Regional variability is huge: From snowpack uncertainty in the Northwest to record capacity prices in PJM.

Download Amperon’s full Winter Weather Outlook for detailed analysis by ISO or watch the Winter Weather Webinar for additional commentary.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

%20(10).avif)

.avif)

.avif)

.avif)

.avif)