MISO’s market just got a major price signal upgrade. With FERC approving an increase in the Value of Lost Load (VOLL) from $3,500/MWh to $10,000/MWh, the cost of unserved energy might get a lot more expensive — at least on paper.

This change, effective September 30th, 2025, gives new meaning to scarcity pricing in the region. It is a drastic move aimed at boosting investment signals for reliability-focused resources — like flexible generation, storage, and demand response — especially as the grid faces mounting pressure from immense load growth and increases in weather volatility.

What is VOLL and Why Does it Matter Now?

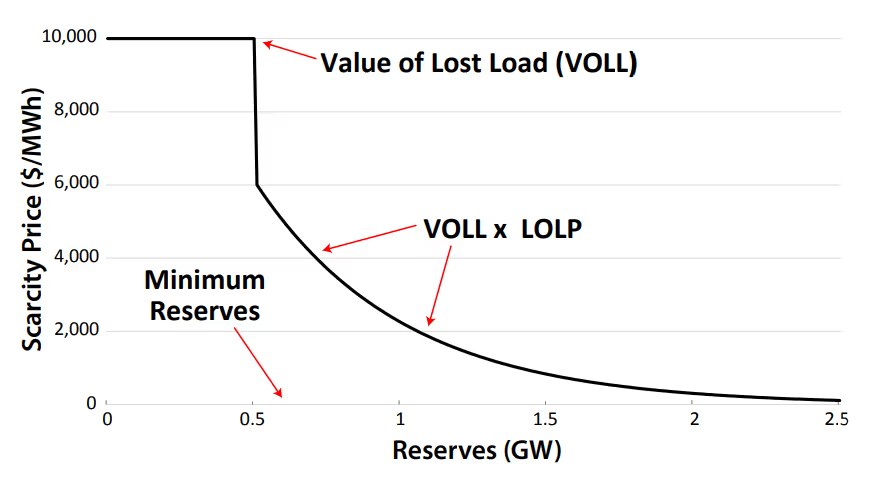

VOLL is an economic estimate of how much electricity customers would be willing to pay to avoid an outage. Think of it as the market’s attempt to quantify the pain of a blackout.

Industrial customers tend to have a high VOLL due to the opportunity cost of lost productivity, whereas residential customers have a much lower opportunity cost. MISO uses this estimate as the top of its Operating Reserve Demand Curve (ORDC), which governs how scarcity prices rise as operating reserves fall. The steeper the curve, and the higher the VOLL, the sharper the price signals during grid stress.

(This ORDC is for visualization and does not reflect the actual values of MISO's ORDC)

With a new VOLL of $10,000/MWh, MISO’s shortage pricing now more closely reflects the true economic impact of firm load shedding. For context: the only recent directed load shed event in MISO occurred during Winter Storm Uri in 2021, when 700 MW of demand was curtailed in MISO South.

It is worth noting that MISO’s VOLL has not been increased since 2007, when it was raised to $3,500. With recent 10–20-year load outlooks skyrocketing due to increased electrification and data centers, this is one of the levers that MISO is pulling to promote investment in reserves, dispatchable generation, and demand response programs. Those who have opposed the change argue that it has the chance to run some smaller market participants out of business in high grid stress situations, and that the capacity market is already an effective enough lever to promote investment within generation.

What This Means for Market Participants

This VOLL increase is not just a theoretical number. It directly affects:

- Real-time prices: The new VOLL sets the price cap for LMPs and market clearing prices during emergencies.

- Storage and flexible generation: Higher scarcity pricing gives clearer signals to developers. If you are building a battery or a peak plant, knowing the payoff potential during extreme events matters, and with it increasing by almost 3x, this will serve as an attractive signal to investors in dispatchable resources.

- Demand response: Commercial and industrial DR becomes more valuable when prices spike — participation could grow as the financial risks of operating at times of high stress increase.

- Capacity market dynamics: Though some argue capacity markets already provide investment signals, FERC pushed back. VOLL is not about ongoing revenue; it is a stress-test value — a marker of how painful unserved load really is.

Implications for Load Forecasting

The new VOLL has major consequences for market exposure. If an LSE is caught short in real-time during a tight grid event, the financial damage could be catastrophic.

- DART spreads become more sensitive as every megawatt counts.

- A missed forecast could mean paying $10,000/MWh on the open market.

- During a VOLL event, an LSE that needs to purchase 10 MW would be subjected to paying $100,000 for those 10 MWs, whereas prior to this change it would have been capped at $35,000.

- Smaller market participants face existential risk in a single load shed scenario.

As real-time prices are becoming more volatile, day-ahead forecasting is even more critical. Not just for savings, but for survival.

The Bigger Picture

As demand rises — especially from data centers and electrification— MISO’s new VOLL signals a more serious approach to grid reliability. FERC and MISO are aligning market mechanics with the real-world costs of outages, presenting a clear invitation for more investment in dispatchable generation and batteries, as well as increasing the need for accuracy in short-term outlooks for LSEs.

But rising demand also brings rising volatility. With a higher market cap now in place, market participants cannot afford to be caught short when prices spike. Just look at these LSEs in ERCOT who didn't survive Winter Storm Uri. While that is an extreme example, even a minor event can lead to financial loss. That is why it is more critical than ever for MISO participants to adopt an energy forecasting solution that was built for whatever regulatory changes arise.

As MISO stares at the looming stress of data center driven load growth, it is not out of the question to expect them to continue to pull more levers to increase investment in generation. Outside of VOLL, we saw capacity prices jump from $30/MW-day in summer 2024 to $666.50/MW-day in summer 2025 within MISO, made by using a reliability-based demand curve to “better reflect value of capacity and resource adequacy risk across seasons.”

MISO rationalized this action by saying it “sends clear and stable investment signals across the system, including to external resources.” As long as the long-term load outlook continues to grow, and surplus continues to shrink, it is safe to assume these levers will be utilized across MISO and the grid at large.

If short-term forecasting is top of mind, contact us to learn how our forecasting solutions can help you stay ahead in a changing market.

.svg)

%20(3).png)

%20(2).png)

%20(1).png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

%20(15).avif)

.avif)

%20(10).avif)

.avif)

.avif)

.avif)

.avif)